by Paul Hoffmeister, Portfolio Manager and Chief Economist

At the end of October, we advised clients that betting markets were expecting Republicans to retake the White House and Senate, and that the biggest election uncertainty was whether they’d be able to hold on to the House of Representatives. Case in point, Polymarket was giving Republicans only a 51% probability to keep the House at the time, compared to 65% and 84% to win the presidency and Senate, respectively. Lo and behold, Republicans breezed through most of Election Night but their toughest challenge was winning the House, where they secured 220 seats for only a 5-seat majority – one of the narrowest in history.

The slim House majority will make President Trump’s economic agenda a little more difficult to implement. Every vote will matter, and some legislators might view this as an opportunity or “leverage” to hold out for their favorite issues. But Administrations that sweep the White House and Congress typically enjoy enough political momentum to craft their preferred legislation early in their term. So, we expect the incoming Trump Administration will get key economic legislation passed and implemented during the first six months of 2025.

President Trump will pursue an economic agenda propelled by tax cuts, making government more efficient and business-friendly, and rebalancing trade flows based on new tariff arrangements.

This agenda will very likely start with making permanent President Trump’s 2017 tax cuts, which notably reduced the corporate tax rate (to 21% from 35%) as well as marginal income tax rates. Given that those tax cuts are scheduled to expire at the end of 2025, this will be important to accomplish quickly; not simply because of their expiry date but also to re-enliven animal spirits in an economy that seems to be slowing at the margin.

At the same time, we expect the new Administration, namely under Elon Musk and Vivek Ramaswamy through the newly created Department of Government Efficiency (“DOGE”), to aggressively pursue its government efficiency agenda. Their objective will be to identify and excise unnecessary government largess, while also eliminating excessive regulatory burdens on the private sector. In some respects, DOGE will be similar to Trump’s first-term deregulation efforts, but with additional emphasis on reducing government expenditures in light of the ever-growing federal deficit.

And, of course, there will be new tariff measures or at least threats thereof; the purpose of which will be to rebalance trade flows in favor of the United States and/or compel foreign countries to act on specific issues. Already, we’ve seen President Trump threaten through social media new tariffs against Canada and Mexico unless those countries assisted with his new immigration agenda.

Of course, China is in Trump’s crosshairs, and we don’t believe that this trade dispute will be resolved anytime soon. If recent events are any indication, then this variable will likely worsen before it improves.

On December 2, the Biden Administration introduced new controls on semiconductor manufacturing equipment and software tools to limit China’s ability to produce advanced semiconductors. The following day, seemingly in retaliation, China announced its own export restrictions against the United States related to dual-use technologies for civil and military use, including controls on rare earth minerals. This was the first time that China specifically targeted certain exports against the United States, as opposed to all countries. These tit-for-tat measures by both sides exemplify the escalating tech trade war.

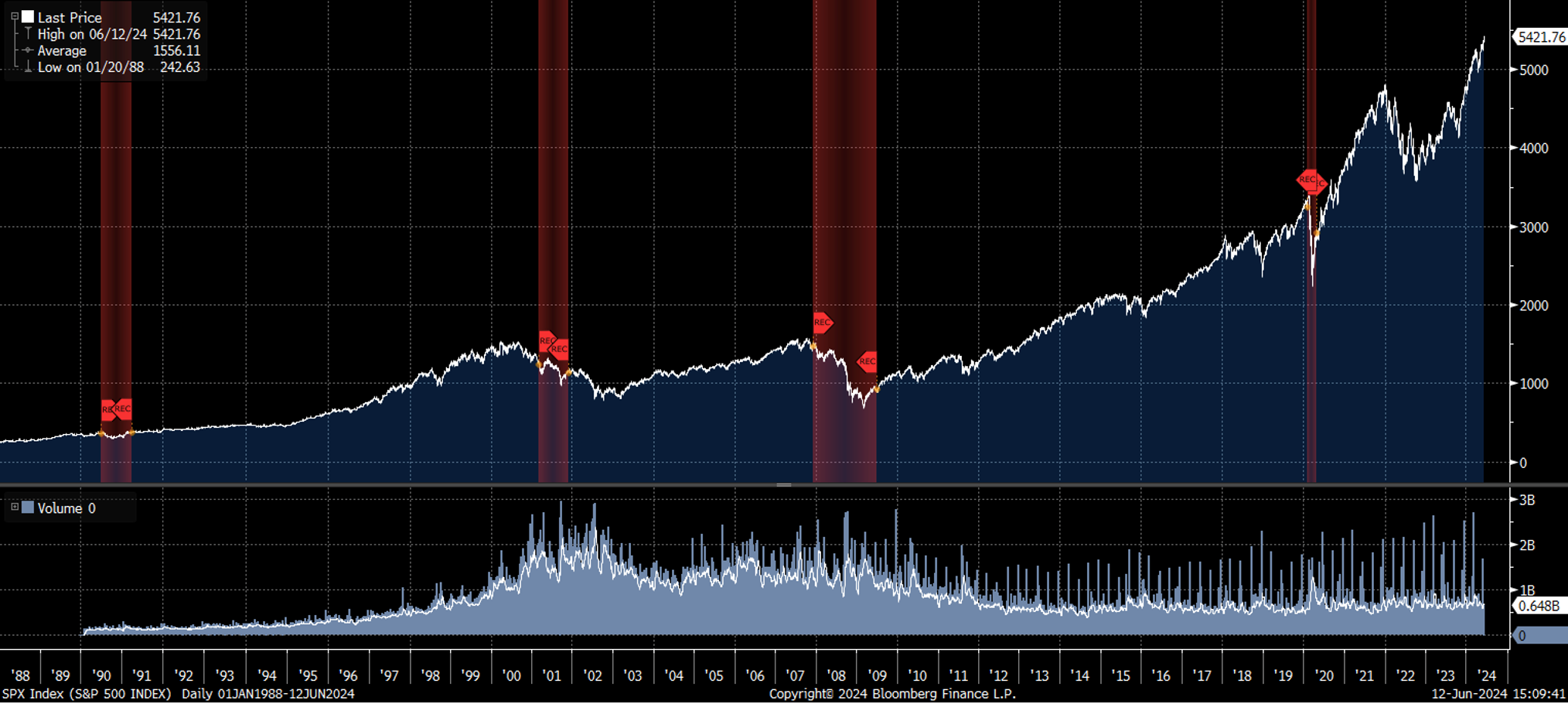

Overall, financial markets appear to view President Trump’s re-election and his economic agenda favorably. Since the close of trading on Monday, November 4 through Tuesday, December 9, the S&P 500 is up +6.0%, Nasdaq +8.6%, and Russell 2000 +7.8%. This business-friendly momentum was only underscored by President Trump’s announcement this week that his Administration will fast track environmental approvals and other permits for any companies investing $1 billion or more in the United States.

Reflecting the investor exuberance today, major equity indices are hitting all-time highs, and credit spreads are historically tight. For example, the extra premium that investors are currently demanding to own Baa-rated corporate bonds over Aaa-rateds is only 61 basis point, according to Bloomberg. Previous times that we’ve seen such a low risk premium (“tight” credit spread) were: early 2005, summer 2014, 2017, and late 2021/early 2022.

At the same time, equity valuations are historically expensive. According to Bloomberg, the S&P 500 has recently traded at a price-to-earnings ratio of more than 25x, compared to a post-1991 average around 20x. In terms of its enterprise value to EBITDA ratio, the S&P has recently traded near 16x, compared to a post-1991 average around 11x.

Indeed, the business outlook looks rosy. Major tax and regulatory relief are on the horizon; the Fed is on a rate-cutting path; artificial intelligence has sparked a tech boom and could be transformational for the economy at large; and by virtue of their aggressive actions in Spring 2023, the Fed has a strong, recent track record of supporting the banking system as some financials navigate the inflation and interest rate surprises of recent years.

But when looking at today’s equity and credit markets through the valuation prism, there’s arguably not a lot of risk being discounted by financial markets today. While it seems counter-intuitive, the rosy outlook has heightened valuations to such a degree that the risk-reward profile is arguably unfavorable for risk assets.

Of course, the business-friendly outlook could be validated in coming months, existing risks might not worsen or new risks might not emerge, and the risk-on environment could therefore continue. So now, with the election uncertainty behind us, the biggest question facing investors might be whether this favorable outlook is sustainable. Given the relatively high equity valuations and tight credit spreads, it seems a lot of things will need to go right next year for investors to once again generate outsized returns.

Paul Hoffmeister is Chief Economist and Portfolio Manager at Camelot Portfolios, managing partner of Camelot Event-Driven Advisors (CEDA), and co-portfolio manager of the Camelot Event-Driven Fund (EVDIX • EVDAX).

Camelot Event-Driven Advisors LLC | 1700 Woodlands Drive | Maumee, OH 43537 // B616

Disclosures:

• Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), will be profitable or equal to past performance levels.

• This material is intended to be educational in nature, and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. Camelot Event Driven Advisors can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

• Any charts, graphs, or visual aids presented herein are intended to demonstrate concepts more fully discussed in the text of this brochure, and which cannot be fully explained without the assistance of a professional from Camelot Portfolios LLC. Readers should not in any way interpret these visual aids as a device with which to ascertain investment decisions or an investment approach. Only your professional adviser should interpret this information.

• Some information in this presentation is gleaned from third party sources, and while believed to be reliable, is not independently verified.

• Camelot Event-Driven Advisors, LLC, is registered as an investment adviser with the United States Securities and Exchange Commission. Registration as an investment adviser does not imply any certain degree of skill or training. Camelot Event-Driven Advisors, LLC’s disclosure document, ADV Firm Brochure is available at http://adviserinfo.sec.gov/firm/summary/291798

Copyright © 2024 Camelot Event-Driven Advisors, All rights reserved.